Introduction

Running a wholesale voice carrier in 2026 is harder than it was two years ago. Margins are thinner, fraud is more sophisticated, FCC Guide-mandated STIR/SHAKEN moved from optional to mandatory in major markets, AI routing displaced the static rate-table model, and POPIA, GDPR, and equivalent frameworks tightened across jurisdictions. The carriers thriving today look different from the ones winning in 2023.

This guide walks through the operational reality of the wholesale voice carrier business — what works, what's broken, where the genuine pressure points sit, and where margin and growth still live. For the buyer-side context, start with what wholesale voice actually is, then come back here for the operator angle.

What Is a Wholesale Voice Carrier Business?

A wholesale voice carrier is a telecom company that buys, sells, and routes voice-call minutes between other carriers, retail providers, and large enterprises. The business sits between Tier-1 infrastructure owners and retail-facing service providers, monetising the gap between bulk capacity rates and per-call termination fees. The global wholesale voice market is projected to surpass $30 billion by 2025, with growth concentrated in convergent voice/messaging platforms rather than pure-play termination shops.

In simpler operational terms: a wholesale voice carrier runs switching infrastructure, maintains interconnect relationships with other carriers, routes calls intelligently across those interconnects, and bills the originating party while paying the terminating party. Margin comes from doing this efficiently at scale — and the underlying mechanics are explained in our pillar on wholesale voice termination.

How a Wholesale Voice Carrier Actually Operates

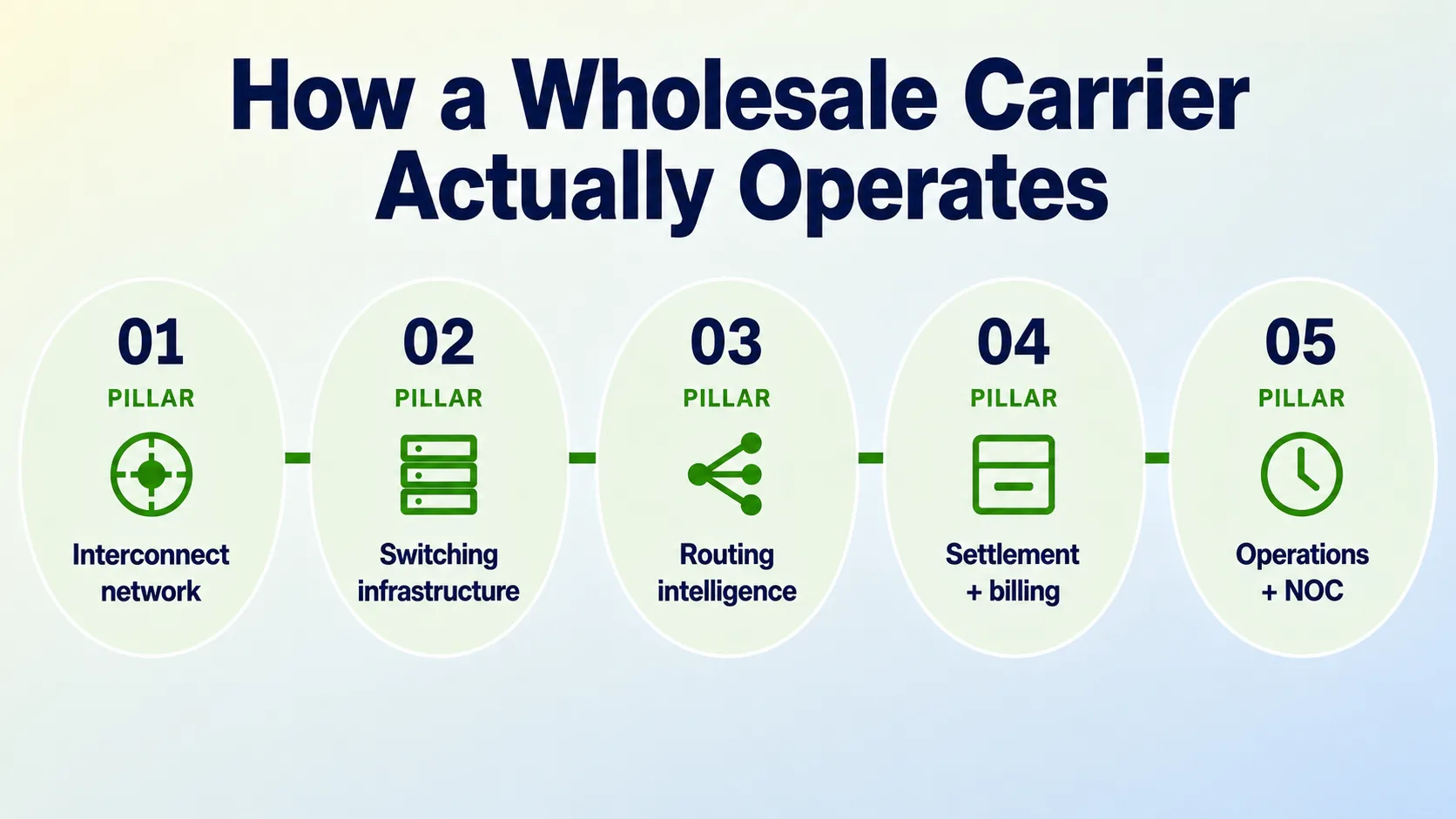

Five operational pillars define a modern wholesale voice carrier — strip out any one of them and what you have is a broker, not a carrier:

- Carrier interconnect network. The carrier maintains direct relationships with telecom operators, mobile network operators, and other wholesale carriers. Quality of these relationships — paid peering, settlement-free peering, transit agreements — determines what destinations the business can reach and at what quality.

- Switching infrastructure. Carrier-grade SIP switches handle call routing in real time. Common platforms include OpenSIPS, Asterisk, FreeSWITCH, and Kamailio for control plane, with hardware switches at the media plane. Geographic redundancy and sub-2-second failover are table-stakes.

- Routing intelligence. Least Cost Routing (LCR) engines pick paths in real time. Modern carriers blend cost-based routing with quality-aware routing — choosing the cheapest path that meets ASR, PDD, and MOS thresholds.

- Settlement and billing. Per-minute billing happens on every leg of every call. CDR generation, reconciliation, and settlement with upstream and downstream partners runs continuously.

- Operations and NOC. 24/7 monitoring of route health, traffic patterns, fraud indicators, and customer escalations. The NOC is where the business actually lives — degraded routes get rerouted, fraud alerts get investigated, customer issues get resolved.

The Real Challenges in 2026

Generic articles list "infrastructure" and "competition" as challenges. The actual operational pressure points are more specific:

Margin compression

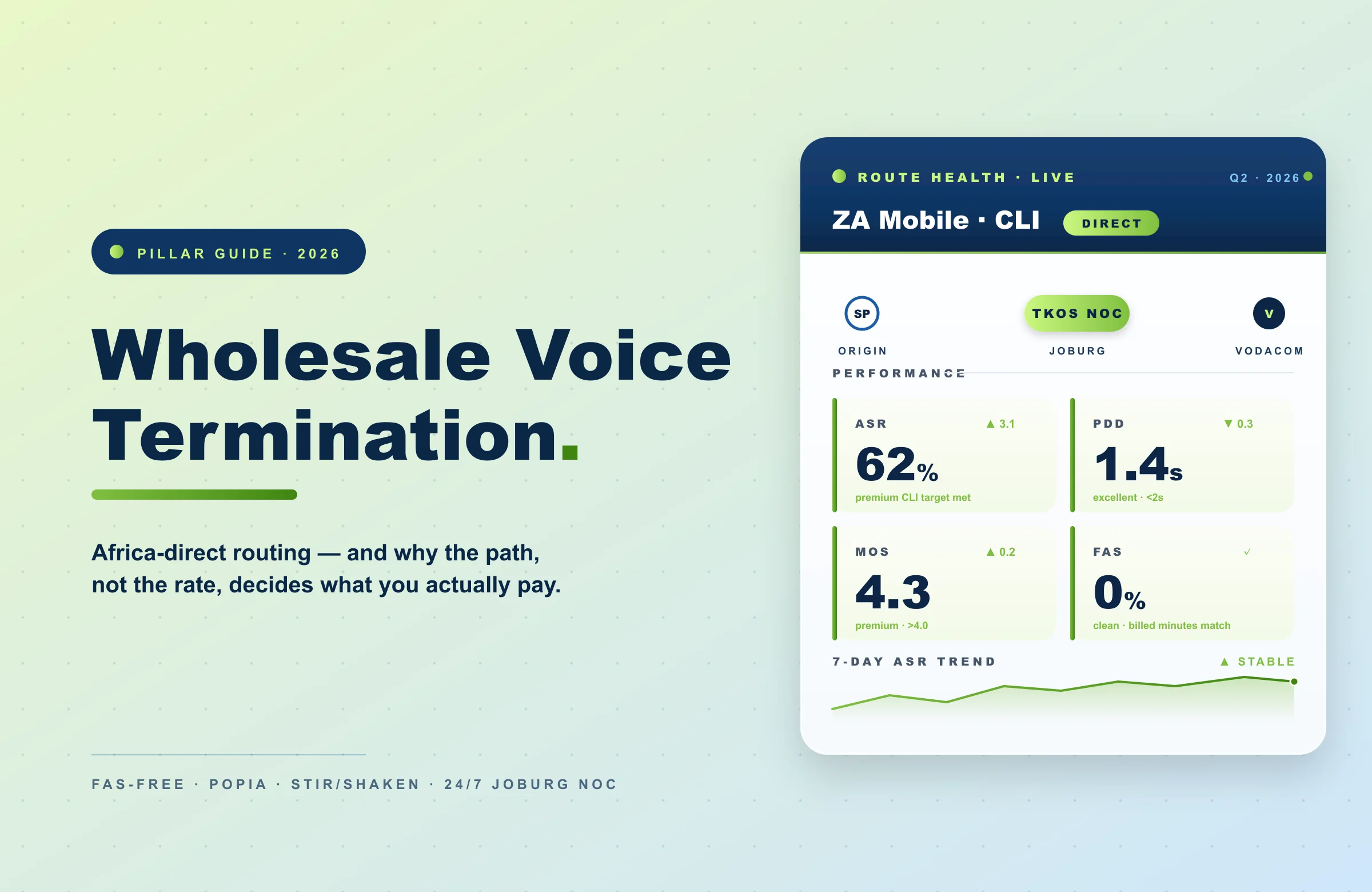

Per-minute wholesale rates have been declining for years across major destinations. Domestic US termination wholesale costs are now under one cent per minute on commodity routes. Operators maintaining margin are doing it through quality differentiation (premium CLI routes, FAS-free billing) and value-added services (real-time analytics, API provisioning), not by competing on raw rate. The race-to-zero on commodity destinations has effectively reset the unit economics, and any platform without a quality story is now competing on volume alone.

Fraud escalation

Three fraud categories dominate carrier loss-reporting:

- International Revenue Share Fraud (IRSF) — fraudsters generate calls to premium-rate numbers they control, splitting the revenue with corrupt insiders. Single events can run into six figures.

- SIM boxing — unauthorised SIMs route international calls through cheap local networks, bypassing international termination rates and stealing revenue from terminating carriers.

- Wangiri (one-ring) fraud — auto-dialed missed calls trigger callbacks to premium-rate numbers. Volume-based, hard to block without false-positives.

AI-powered traffic anomaly detection isn't optional anymore. Carriers running purely rule-based fraud systems are exposed to losses that erase quarterly margin in a single event. Industry-grade telemetry, shared threat intelligence (see the GSMA fraud and security programmes for a sense of the cross-operator coordination involved), and ML anomaly scoring are now baseline operational requirements.

Compliance complexity

STIR/SHAKEN moved from voluntary to mandatory for US-bound traffic. POPIA enforcement in South Africa is active. GDPR continues to evolve. India's DPDP Act creates new constraints. A carrier handling cross-border traffic now needs compliance frameworks that work across jurisdictions — not because compliance is sexy, but because non-compliance gets traffic blocked or fined. The procurement teams at large enterprise buyers now ask compliance questions before they ask about pricing, and the answers feed straight into the vendor scorecard.

Legacy system drag

Most carriers run a mix of modern SIP-based switching and legacy SS7 / TDM gear. Integrating new AI routing, real-time analytics, and API-driven provisioning across that mixed estate is genuinely difficult. The carriers moving fastest in 2026 are the ones who invested in cloud-native switching architecture earlier — they have less legacy debt to drag through every upgrade cycle.

What's Working in 2026

Four engineering investments separate the operators gaining share from the ones losing it. Each one shows up on the P&L within two quarters of being deployed at scale, and each one compounds — better routing produces better data, which trains better fraud models, which raises ASR and ACD, which lets the platform charge a premium without losing volume.

AI-powered routing

Static LCR is being displaced by quality-aware, predictive routing. Machine learning models forecast which routes will perform on which destinations at which times of day, based on real-time ASR, PDD, and MOS telemetry. Calls get routed to the path most likely to complete cleanly — not just the cheapest path that's nominally available.

Cloud-native switching

Cloud-based softswitches deployed across multiple geographic regions deliver redundancy without the capital expense of physical infrastructure. Carriers spinning up additional capacity to handle traffic surges (or failing over from a degraded region) do it in minutes instead of weeks. The economic model fundamentally favours cloud over on-premise for new buildouts.

Real-time analytics and API control

Buyers of wholesale voice now expect real-time visibility into their traffic — per-route ASR, per-destination ACD, per-time-window performance trends. Carriers offering REST APIs for provisioning, routing changes, and CDR access win against those still operating through email and ticket queues. "API-first" is now table-stakes for carrier sales to enterprise and CPaaS buyers.

Compliance as a product feature

Carriers that built compliance into the platform — STIR/SHAKEN attestation, POPIA-aligned data handling, GDPR-ready CDR retention, HIPAA-configurable infrastructure — are winning the deals where compliance audit is part of the procurement process. Non-compliant carriers either lose the deal or accept regulatory risk neither party can afford.

The African Wholesale Voice Carrier Market in 2026

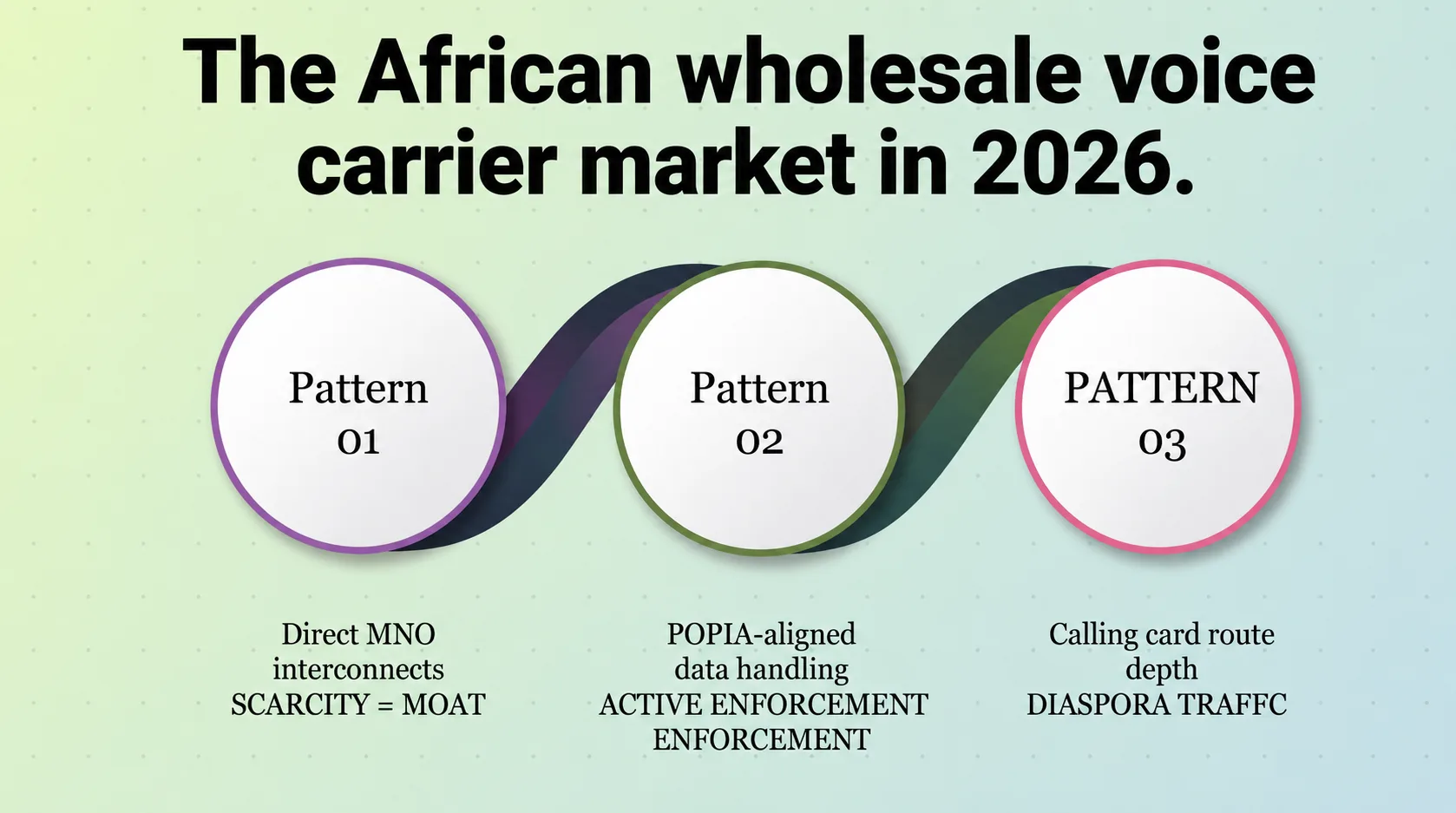

African voice traffic deserves separate treatment. The continent's market dynamics differ meaningfully from European or US wholesale voice — and most global articles ignore them entirely. For any wholesale voice carrier with serious African ambitions, three patterns matter more than the global rate sheet:

- Direct interconnect scarcity. Most global wholesale carriers don't have direct relationships with major African MNOs (Vodacom, MTN, Cell C, Telkom, Safaricom). They route African traffic through European or US aggregators, adding hops and degrading quality.

- POPIA enforcement. South Africa's Protection of Personal Information Act has been in active enforcement since July 2021. Carriers handling South African traffic must comply with POPIA data handling — most global providers offer GDPR but not POPIA.

- Calling card volume. African destinations remain a major calling card market, particularly outbound calling card traffic from diaspora populations. Specialised CC routes for African destinations are a meaningful business segment most global carriers don't optimise for.

How a Wholesale Voice Carrier Wins in 2026

Five priorities define the operators thriving in the current environment — each one moves the business away from rate-card competition and toward defensible quality and developer experience:

- Quality differentiation over rate competition. FAS-free billing, premium CLI routes with measurable ASR, contractual uptime SLA — sell these, not the cheapest per-minute rate.

- AI-driven routing and fraud detection. Static rule-based systems are being out-performed in cost and quality. ML-driven traffic optimisation and anomaly detection are now baseline.

- Direct interconnects in differentiated destinations. Owning relationships in markets others aggregate (Africa, parts of LATAM, parts of South Asia) creates margin that commodity destinations don't.

- Compliance as a product. STIR/SHAKEN, POPIA, GDPR, HIPAA — engineered into the platform, not retrofitted. Compliance is a sales advantage, not a cost.

- API-first customer experience. Self-service portal, REST API for everything provisioning, real-time CDR access. Buyers who can build on top of you stay longer than buyers who can't.

Conclusion

The wholesale voice carrier business in 2026 is no longer a rate-table game. The carriers earning durable margin are the ones investing in AI-driven routing, ML-based fraud detection, cloud-native switching, API-first customer experience, and compliance engineered into the platform across STIR/SHAKEN, POPIA, GDPR, and HIPAA.

Africa-anchored operators with direct MNO relationships hold a structural moat that commoditised destinations don't offer. Looking forward, expect the gap between engineered wholesale voice carrier platforms and brokers running spreadsheets to widen — the next two years will reward operators who treat compliance, quality, and developer experience as products, not as overhead.