Introduction

Wholesale voice is one of those terms the telecom industry repeats often and explains rarely. Every international call you place, every contact-centre dial, every cloud phone ring rides on top of it — yet the layer itself stays invisible to the people who depend on it. This guide opens the curtains.

We will define wholesale voice, walk through who buys it and who sells it, follow the money across the carrier hierarchy, explain why African routing is engineered differently, and lay out the quality metrics that actually predict whether a call connects. No marketing fog, just the working mechanics. For the operator angle, see how TKOS handles wholesale voice.

What Is Wholesale Voice? A Plain Definition

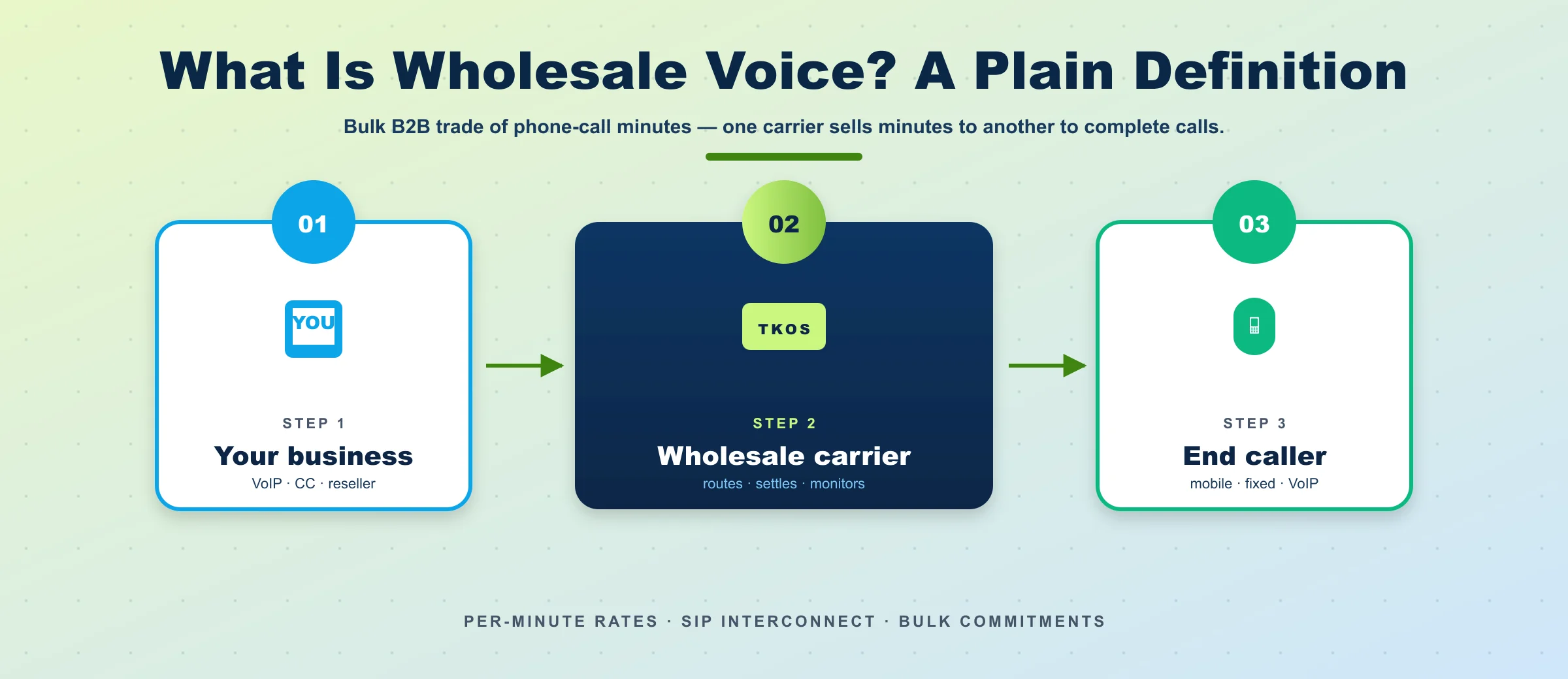

Wholesale voice is the bulk B2B trade of phone-call minutes between telecom carriers. One carrier sells minutes to another to complete calls into networks they don't own.

It's the layer where retail providers, mobile operators, and VoIP wholesalers buy the routing capacity they resell as consumer or business phone service. Three terms get used interchangeably and shouldn't be:

- The market and the service category itself.

- A carrier — a company that sells these minutes (TKOS is one).

- Voice termination — the specific act of completing a call on the destination network. Termination is what you buy when you buy the service.

Tier 1, Tier 2, Tier 3 — Who Owns the Network

Wholesale voice runs on a three-tier carrier hierarchy. Knowing where a provider sits explains a lot about their pricing and what they can actually deliver.

Tier-1 Carriers

Tier-1 carriers own physical telecom infrastructure — undersea fiber, mobile towers, central offices, satellite uplinks. AT&T, Verizon, Orange, Deutsche Telekom, BT, MTN, Vodafone are Tier-1 names. They have settlement-free peering with each other: when AT&T sends a call to BT, no money changes hands. Tier-1 carriers are the only ones who own the actual roads.

Tier-2 Carriers

Tier-2 carriers own significant infrastructure but pay Tier-1 carriers to transit traffic into networks they don't reach directly. Most regional carriers and international VoIP wholesalers operate at Tier-2, with direct interconnects to some destinations and resold access to others.

Tier-3 Carriers

Tier-3 carriers own minimal infrastructure and lease most of their capacity from Tier-2 and Tier-1 partners. The advantage is flexibility; the disadvantage is full dependency on upstream carrier relationships.

TKOS operates as a hybrid. Direct carrier relationships across South Africa, Africa, and key global hubs put us at Tier-2 for African traffic, with Tier-1 partner relationships for destinations where direct interconnects aren't economical. See the deep-dive on operating a wholesale voice carrier for how this layer actually runs. "Pure Tier-1" is mostly a marketing claim.

How Money Moves Through Wholesale Voice

Every minute is split between three or four parties. The chain looks predictable until you trace where each cent actually lands.

The economics are simple if you've sold anything by the unit. A retail customer places a call and pays a retail rate, say 50 cents per minute international. The retail provider hands the call off to a wholesale voice carrier through a SIP trunk at roughly 8 cents per minute. The carrier picks the best path using Least Cost Routing and pays a Tier-1 partner around 5 cents to terminate. The Tier-1 partner hands the call to the destination carrier, which charges its own settlement rate, often regulated by the local telecom authority. Every party bills the previous party and takes a margin.

Run that retail 50 cents through the chain and the split typically lands somewhere near 30 cents to retail margin, 8 cents to the wholesale layer, 5 cents to the Tier-1 transit, and 7 cents to the terminating carrier. Adjust the destination, the route quality, and the volume commitment, and the same minute can earn or burn margin at every hop.

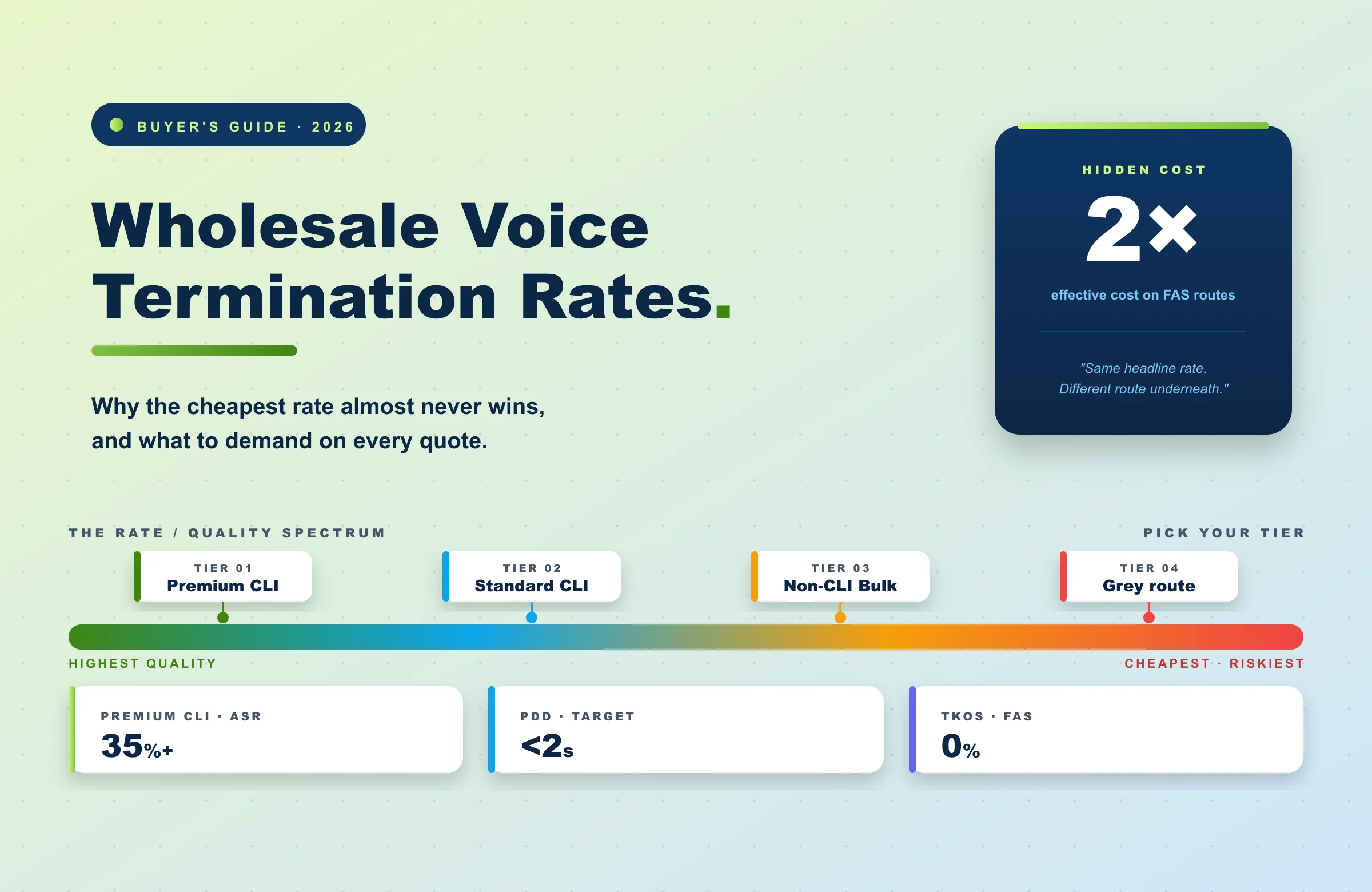

That's why the cheapest rate isn't always the best rate. A 5-cent route might have higher fraud exposure, lower answer rates, or pass calls through three Tier-3 intermediaries before they actually terminate. Each hop is another chance for quality to degrade — and another place where False Answer Supervision (FAS) inflation can quietly siphon revenue. The full margin equation includes call quality, completion rate, and FAS exposure — for the full breakdown see our pillar on wholesale voice termination.

The lesson most carriers learn the expensive way: model total cost per connected minute, not headline per-minute. A clean route at a slightly higher rate almost always beats a cheap route polluted with FAS, dropped calls, and spam-flagged caller IDs.

Peering — The Word Everyone Uses Wrong

Peering means two carriers exchange traffic directly, without a third party in between. Settlement-free peering is rare and almost always Tier-1 only — both sides send roughly equal traffic, so neither bills the other. Paid peering is more common: one carrier pays the other for direct interconnect, usually because one side sends more traffic than it receives. Many "direct relationships" carriers advertise are paid peering arrangements. That's still better than transit — fewer hops, lower latency, more accountability — but it isn't free. (For the formal definition, see the peering article on Wikipedia.)

Why African Voice Traffic Is Routed Differently

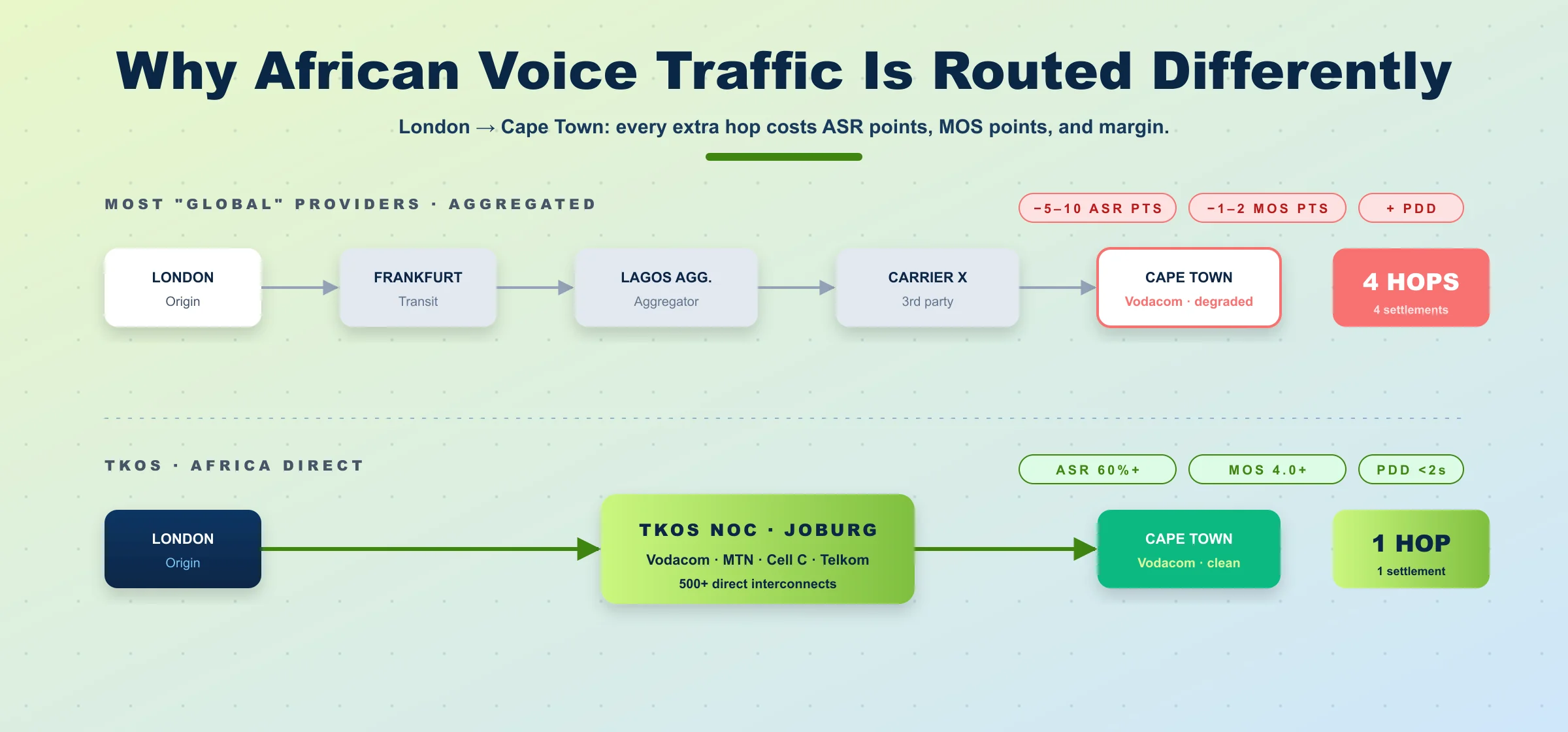

When a call from London to Cape Town terminates on Vodacom, the physical path matters. One hop into Africa is the goal — every extra hop costs quality.

Most "global" VoIP providers route through a Frankfurt or Lagos aggregator first — two hops, two settlements, latency added at each. A direct path from a wholesale carrier with a Vodacom interconnect is one hop, one settlement, original quality preserved.

This matters in numbers, not just architecture. Aggregated routes into Africa typically deliver 5—10 percentage points lower Answer Seizure Ratio (ASR) than direct routes, plus higher Post-Dial Delay and a wider spread on voice quality scores. Across thousands of monthly minutes, those gaps mean real revenue.

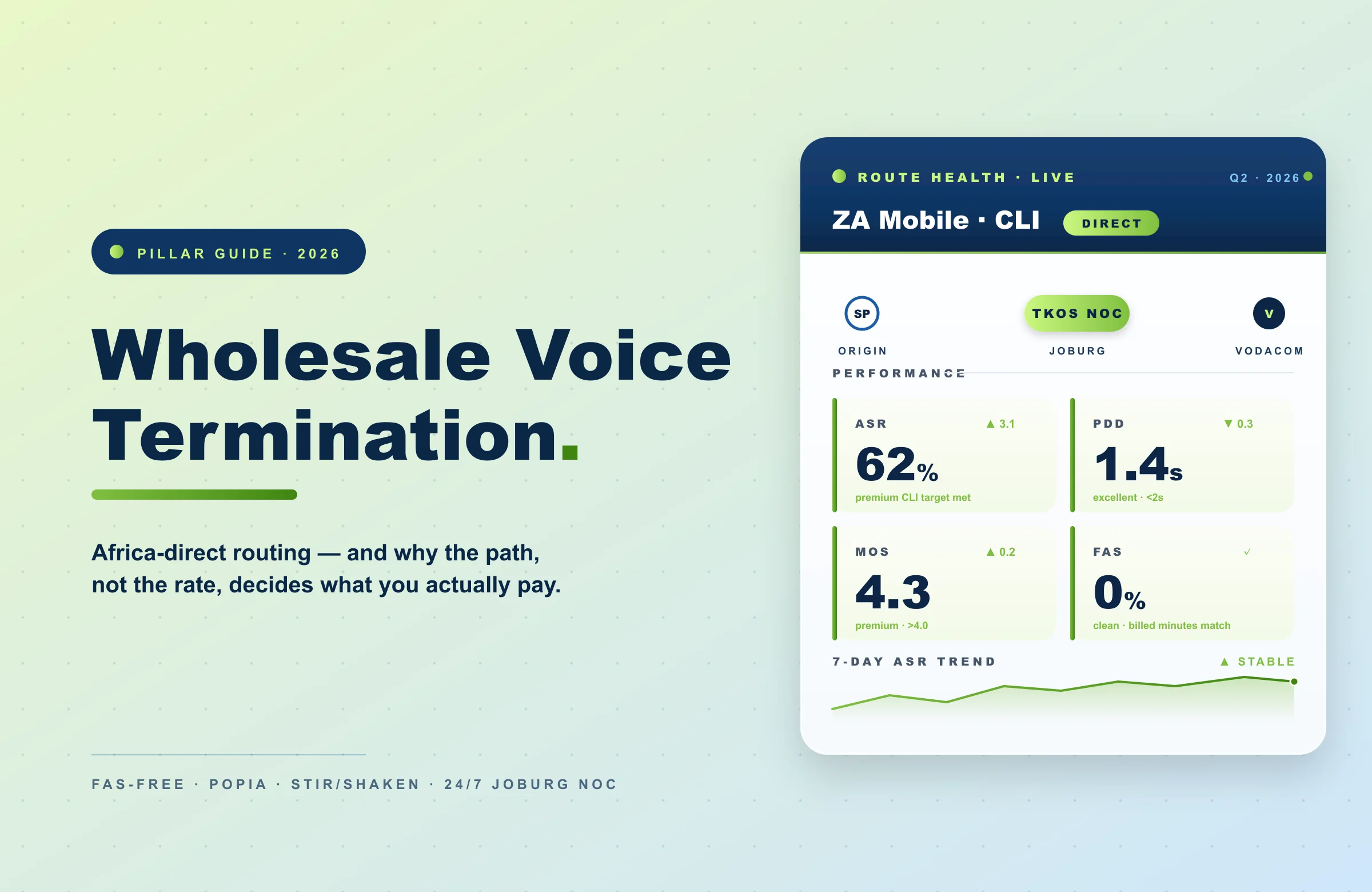

The Johannesburg-anchored network at TKOS exists for this reason. Direct relationships with major African mobile network operators — Vodacom, MTN, Cell C, Telkom — and a tier-3 NOC sitting in South Africa mean traffic into the continent doesn't get aggregated through someone else's data centre.

Who Actually Buys Wholesale Voice?

The buyer is almost never an individual. Five categories cover most of the market, and each one buys the service for slightly different reasons:

- Retail VoIP providers — RingCentral, Zoom Phone, Vonage and every cloud phone system rely on wholesale capacity underneath. Their margin is the spread between the wholesale rate and what they charge end users.

- Mobile network operators — even Tier-1 carriers buy capacity for international destinations they don't reach directly. South African operators routing to Australia, US carriers terminating to Eastern Europe, Indian carriers handling US-bound traffic.

- CPaaS platforms — Twilio, Plivo, MessageBird, Vonage API. Programmable communications run on this infrastructure. When a developer's app makes a call, that call hits a wholesale carrier within milliseconds.

- Contact centres and outbound dialers — large operations buy direct to keep per-minute costs down. A 200-seat outbound centre dialling thousands of calls per hour saves substantially against retail VoIP pricing.

- Calling card operators — specialised CC routes optimised for African and South Asian destinations, where calling card volume remains highest and the routing engineering is unique to those traffic patterns.

“Once you understand who's actually buying minutes, the rate sheet stops looking like a price list and starts looking like a portfolio of risks and obligations.”

TKOS network engineering team

What's Changing in 2026

The wholesale voice market is projected to surpass $194 billion by 2027. Four shifts are reshaping how the industry operates:

- AI routing displacing static LCR. Real-time MOS scores, ASR forecasts, and carrier performance trends now drive path selection.

- STIR/SHAKEN expanding beyond the US. The FCC Guide mandated caller authentication for US originations in 2021. Canada, parts of Europe, and select APAC markets are now adopting equivalent frameworks.

- Regional compliance tightening. POPIA in South Africa, the DPDP Act in India, evolving GDPR enforcement in the EU. Compliance has to be built into the platform, not bolted on.

- Convergence with messaging and number management. Buyers want one provider for voice termination, virtual numbers, and bulk SMS — not three vendor relationships.

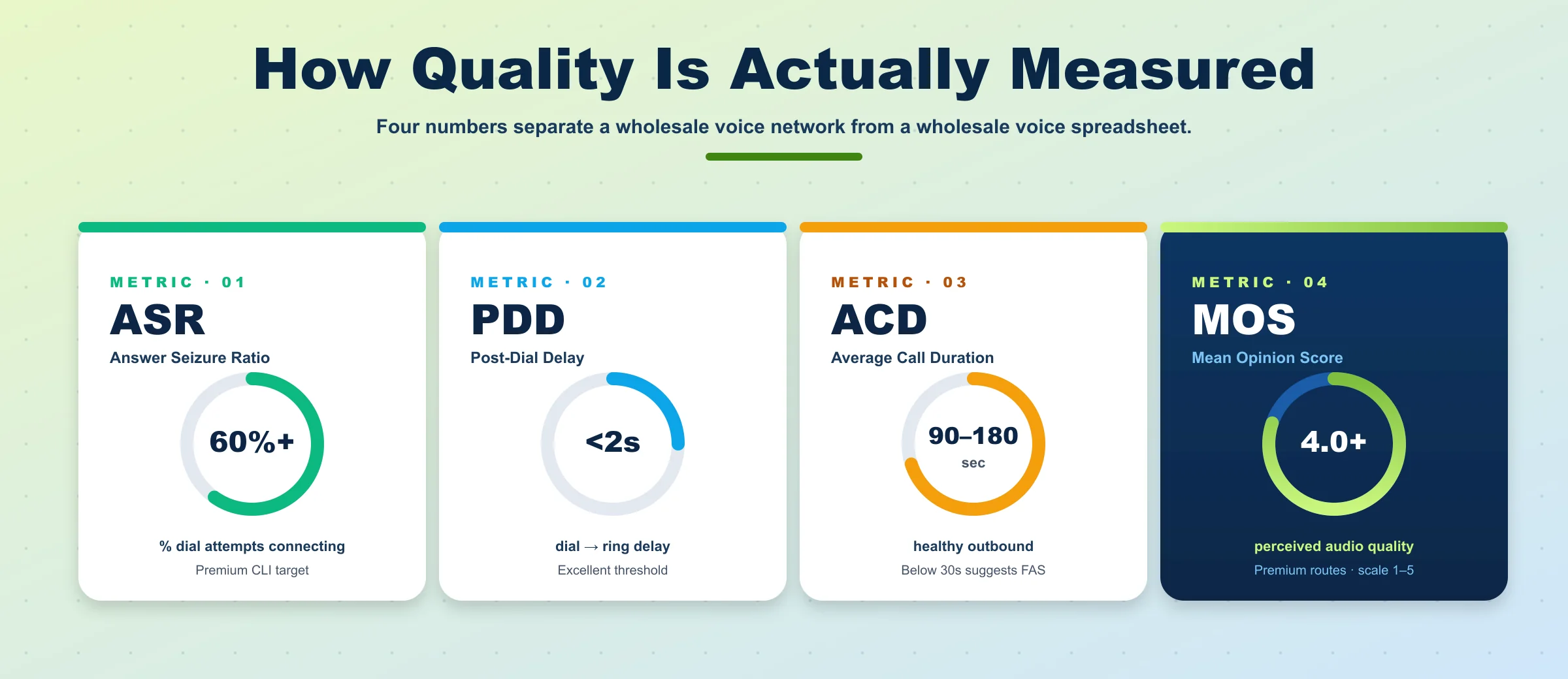

How Quality Is Actually Measured

Four numbers matter more than the per-minute rate. Together they tell you whether a route is healthy or quietly bleeding revenue.

- ASR — Answer Seizure Ratio — % of dial attempts that connect. Pure CLI: 60%+.

- PDD — Post-Dial Delay — time between dialing and ringing. Under 2 seconds excellent.

- ACD — Average Call Duration. Healthy: 90—180s. Below 30s suggests FAS.

- MOS — Mean Opinion Score — voice quality from 1 to 5. Premium: 4.0+.

A provider that can't deliver these numbers per route, per destination, in real-time is running a black box. One with proper analytics shows you exactly how each route performs — and lets you switch traffic when one degrades.

Conclusion

Wholesale voice is not a magical backbone — it is a real B2B market governed by carrier tiers, peering economics, settlement flows, fraud risk, and a small set of measurable quality signals. The buyers who win in 2026 are the ones who stop shopping on per-minute rate alone and start treating ASR, PDD, ACD, MOS, and FAS exposure as the real currency.

They pick partners with direct interconnects into the destinations that matter to their traffic, audited compliance across jurisdictions, and analytics they can actually act on. Looking forward, AI routing, multi-product convergence, and regional compliance will keep raising the bar — and the operators that engineer for those shifts now will be the ones still standing in 2027.