Introduction

Picture an MSP that sold $40K of voice services last quarter and is wondering whether to launch its own wholesale VoIP business. The economics look attractive on paper. The infrastructure looks expensive in reality. Somewhere between those two views sits the operational truth: running a carrier business is harder than the rate sheets suggest and more lucrative than the marketing fluff implies — but only if you get five things right.

This guide breaks down how the business actually operates, where margin really comes from, the operational pressure points that separate profitable carriers from struggling ones, and where the white-label model fits for buyers who want carrier economics without building infrastructure from scratch. It's written for MSPs, resellers, and platform builders evaluating whether to enter — or stay in — the market.

How the Business Actually Operates

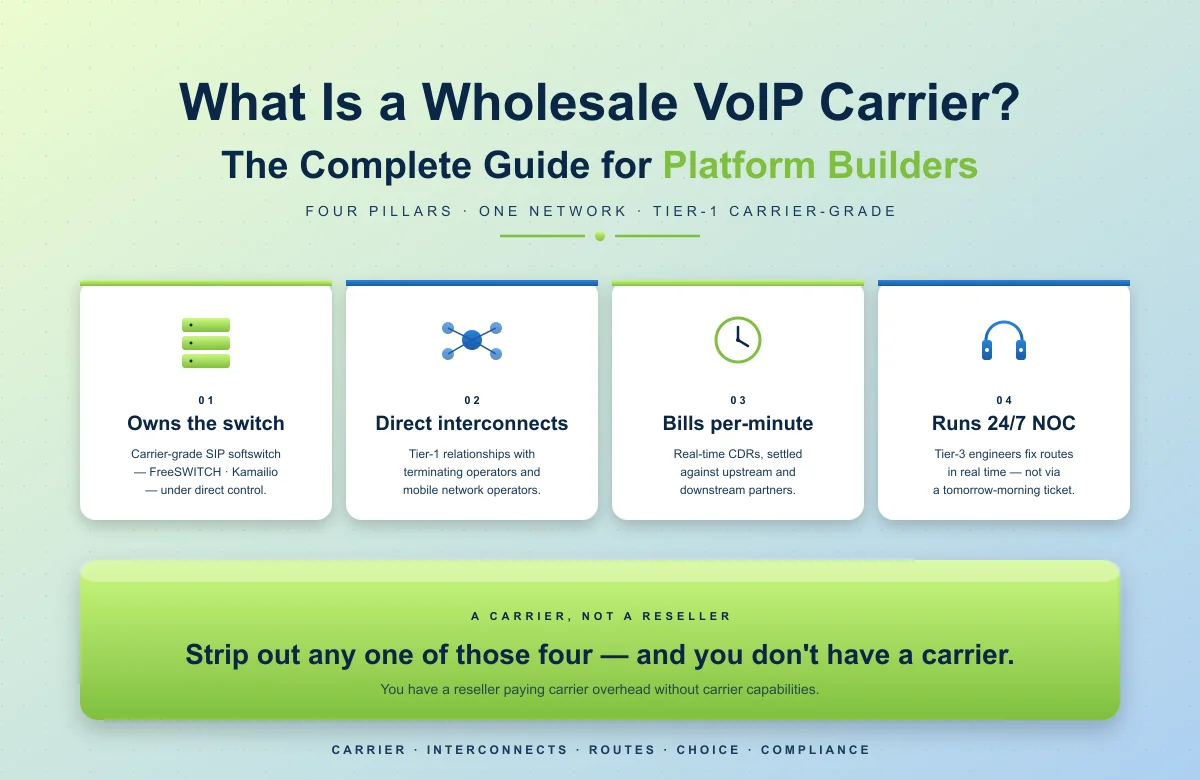

Five operational pillars define every functional carrier:

- Carrier interconnect network. Direct relationships with terminating operators, mobile network operators, and other wholesale carriers. The depth of this network determines reach and quality.

- Switching infrastructure. Carrier-grade SIP softswitches (FreeSWITCH, OpenSIPS, Kamailio, Asterisk) handle real-time routing. Geographic redundancy with sub-second failover is the baseline.

- Routing intelligence. Least Cost Routing engines pick paths in real time, balanced against quality-aware routing that factors in ASR, PDD, and MOS thresholds.

- Settlement and billing. Per-minute billing on every leg of every call. CDR generation, reconciliation, and settlement runs continuously across upstream and downstream partners.

- Operations and NOC. 24/7 monitoring of route health, traffic patterns, fraud indicators, and customer escalations. The NOC is where the business actually lives.

Strip out any one and you don't have a carrier. You have a reseller paying carrier overhead without carrier capabilities. The same dynamic applies to wholesale voice termination buyers evaluating whether their upstream actually owns the switch.

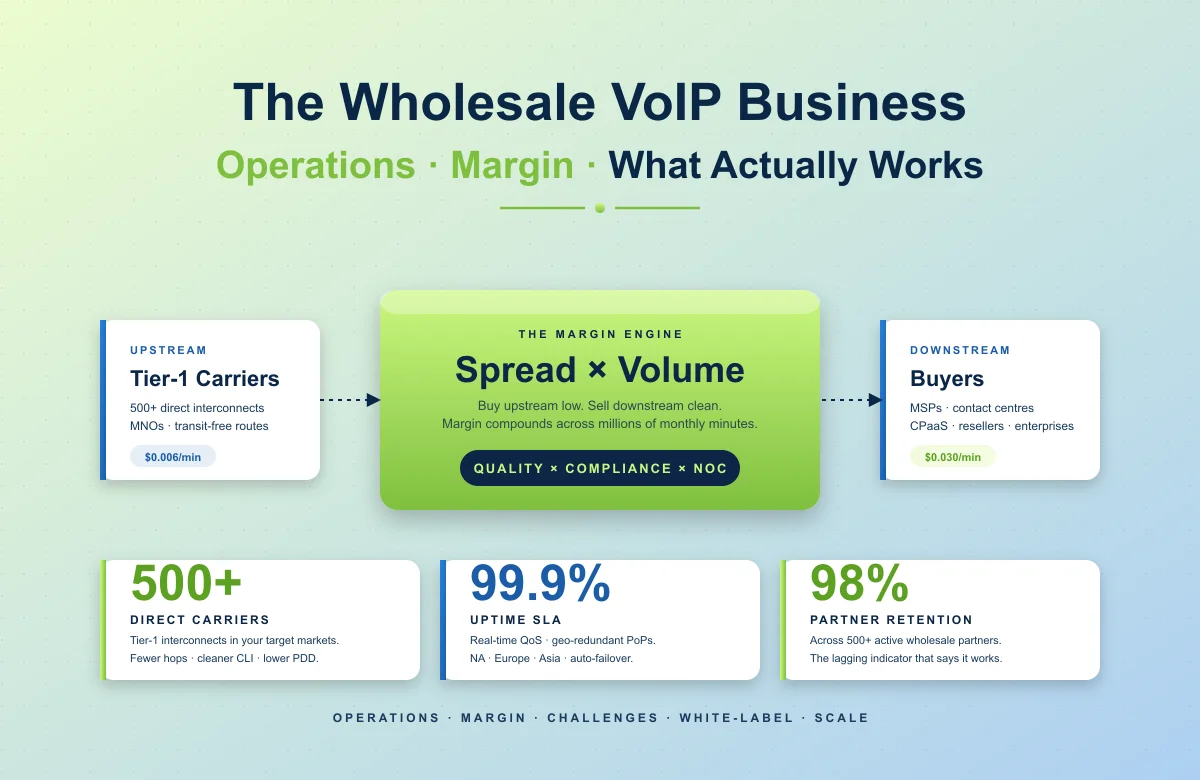

Where Margin Actually Lives

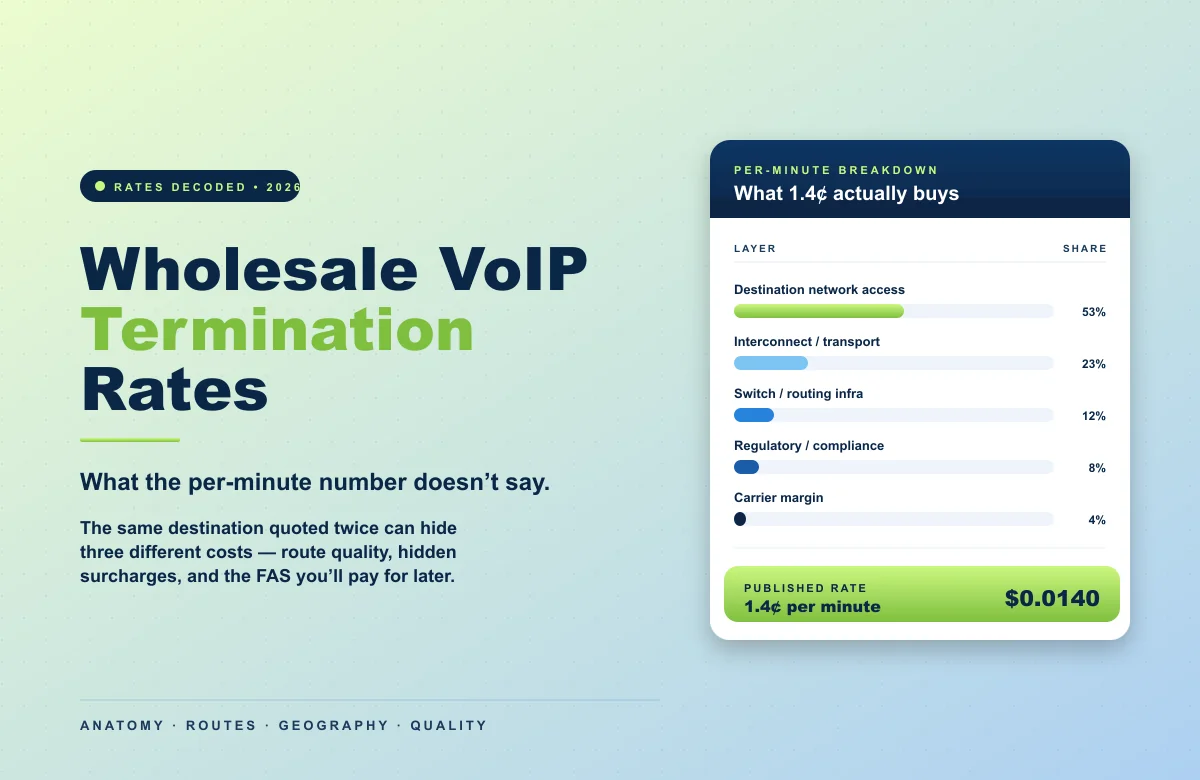

Per-minute wholesale rates have been declining for years across major destinations, a trend documented in GSMA wholesale telecom market data. Domestic US termination is now under one cent per minute on commodity routes. Margin in the carrier business doesn't come from charging more for the same minute. It comes from doing the minute better.

Quality differentiation drives premium rates. Premium CLI routes, FAS-free billing, contractual ASR — buyers pay more for these because they convert directly into completion rates and customer trust. Africa-direct interconnects command meaningful premiums because most global carriers route African traffic through transit aggregators with worse quality.

Value-added services extend margin further. Real-time analytics through APIs, self-service provisioning, white-label portals, compliance-as-a-feature (HIPAA, FCC Guide-mandated STIR/SHAKEN attestation) — these turn a commodity per-minute business into a recurring-revenue platform that competitors can't easily replicate.

The Real Operational Challenges

Generic articles list "infrastructure" and "competition" as challenges. The actual operational pressure points are more specific:

Margin compression. Commodity rates keep falling. Carriers maintaining margin do it through quality differentiation and value-added services, not by competing on raw rate.

Fraud escalation. IRSF, SIM-box bypass, and wangiri callbacks generate single-event losses that erase quarterly margin. AI-powered traffic anomaly detection isn't optional anymore.

Compliance complexity. STIR/SHAKEN moved from voluntary to mandatory for US-bound traffic. Cross-border traffic now needs compliance frameworks that work across multiple jurisdictions.

Legacy system drag. Most carriers run a mix of modern SIP and legacy SS7/TDM gear. Integrating new routing intelligence and analytics across that mixed estate is genuinely difficult.

Capital intensity. Direct interconnects, redundant switching, and a 24/7 NOC require sustained investment. The business rewards scale; small carriers struggle to amortise overhead.

Why the White-Label Model Works

For MSPs, resellers, and platform builders, building a carrier from scratch usually doesn't pencil. The white-label model — running a branded voice service on top of someone else's carrier infrastructure — does. Done right, it gives you the margin profile of a carrier without the capital expense.

The trade-off is that you're trusting the underlying carrier with everything that matters: route quality, FAS exposure, fraud protection, NOC response time. A bad carrier underneath turns your branded voice service into a complaint queue. A good one disappears into the background while your unit economics improve.

Why Africa-Focused Operators Look Different

African voice traffic is the most fragmented termination market on the planet. Direct interconnects with major African MNOs (Vodacom, MTN, Cell C, Telkom, Safaricom) are scarce among non-African wholesalers. Most US and European wholesale providers route African traffic through transit partners — three or four hops minimum on most routes.

That gap is a margin opportunity for operators with direct African relationships. TKOS operates from a Johannesburg-anchored network with carrier relationships built across the continent over a decade. The economics work because direct interconnects deliver quality the transit market can't match — and buyers pay accordingly.

How TKOS Powers This Business Model

Whether you're running your own wholesale VoIP business or building a white-label service on top of carrier infrastructure, TKOS delivers the network underneath:

- 500+ direct carrier interconnects for fewer hops and superior audio clarity.

- Geographically redundant architecture with PoPs in North America, Europe, and Asia plus automatic failover.

- 99.9% uptime SLA backed by real-time QoS monitoring at the NOC.

- CLI, Non-CLI, and A-Z routes — FAS-free as a baseline.

- STIR/SHAKEN active for proper US-bound attestation.

- HIPAA-compliant voice for healthcare clients and partners.

- 100+ countries DID coverage for white-label local presence.

- 24/7/365 NOC with tier-3 engineers — issues resolved on the first call.

- White-label provisioning for MSPs and resellers running branded voice on top of TKOS infrastructure.

98% partner retention across 500+ active partners reflects what this business model looks like when the carrier underneath actually works.

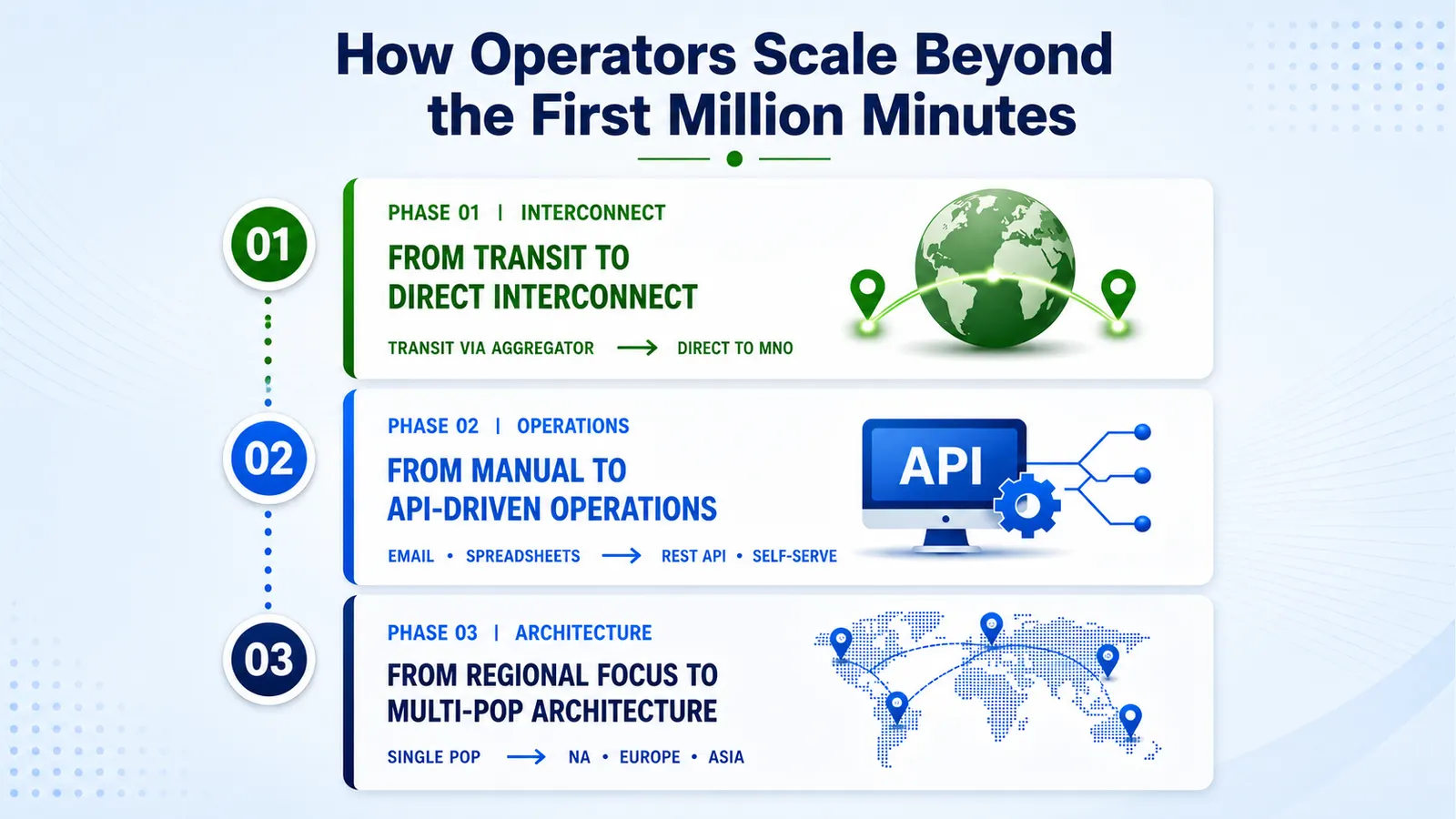

How Operators Scale Beyond the First Million Minutes

This business model rewards scale, but the path from a few hundred thousand minutes to multi-million-minute volumes isn't linear. Three transitions matter:

- From transit to direct interconnect. Early-stage carriers often buy capacity from larger wholesalers. Hitting volume thresholds with destination operators unlocks direct interconnect agreements that improve quality and margin simultaneously.

- From manual to API-driven operations. Provisioning routes by email and adjusting rate sheets in spreadsheets stops scaling around half a million monthly minutes. Real wholesale VoIP businesses move provisioning, CDR access, and rate management into APIs once volume justifies the engineering investment.

- From regional focus to multi-PoP architecture. Single-PoP carriers carry concentration risk and latency penalties. Multi-region PoPs (NA, Europe, Asia) reduce both. Most successful operators cross this threshold around the multi-million-minute mark.

TKOS infrastructure already covers all three transitions. White-label partners running on TKOS skip the buildout and inherit the scale-ready architecture from day one.

What Successful Operators Get Right

Across the carriers that maintain margin and grow, four practices repeat. They invest in direct interconnects in markets others aggregate, treating regional depth as a moat. They build compliance into the platform rather than retrofitting it. They publish per-route quality data — ASR, PDD, FAS exclusion — and treat transparency as a competitive advantage. Top operators staff the NOC with engineers who can solve problems on the first call instead of routing tickets through tiers. None of these are technology choices. They're cultural ones, and they're what separates a profitable operator from a struggling one.

Conclusion

The wholesale VoIP business rewards depth over breadth — direct interconnects in markets others aggregate, compliance built into the platform, transparent quality data, and a NOC that resolves issues on the first call. Carriers that build their wholesale VoIP business on those four practices grow margin while commodity rates compress around them. The white-label model lets MSPs and resellers capture the same wholesale VoIP business economics without the capital expense.

Getting Started

If you're evaluating whether to launch a wholesale VoIP business — or whether to switch the carrier under your existing one — start with the carrier-economics questions: route quality, FAS exposure, NOC response, compliance posture. The rate sheet comes after.